Financial rationale

The rapid rise of AI has sparked fears about its role in the next financial crisis (Financial Times—Editorial Board, 2023). Some worry trading algorithms could trigger a crash; others fear an AI bubble could burst, dragging global markets down.

The substantial investments by major corporations in AI offer new opportunities, yet they also increase integration, hence raising systemic risk. While many of these companies have been presenting in recent years steady financial results, the risk of another tech bubble like the 2 000 dot-com bubble cannot be ignored.

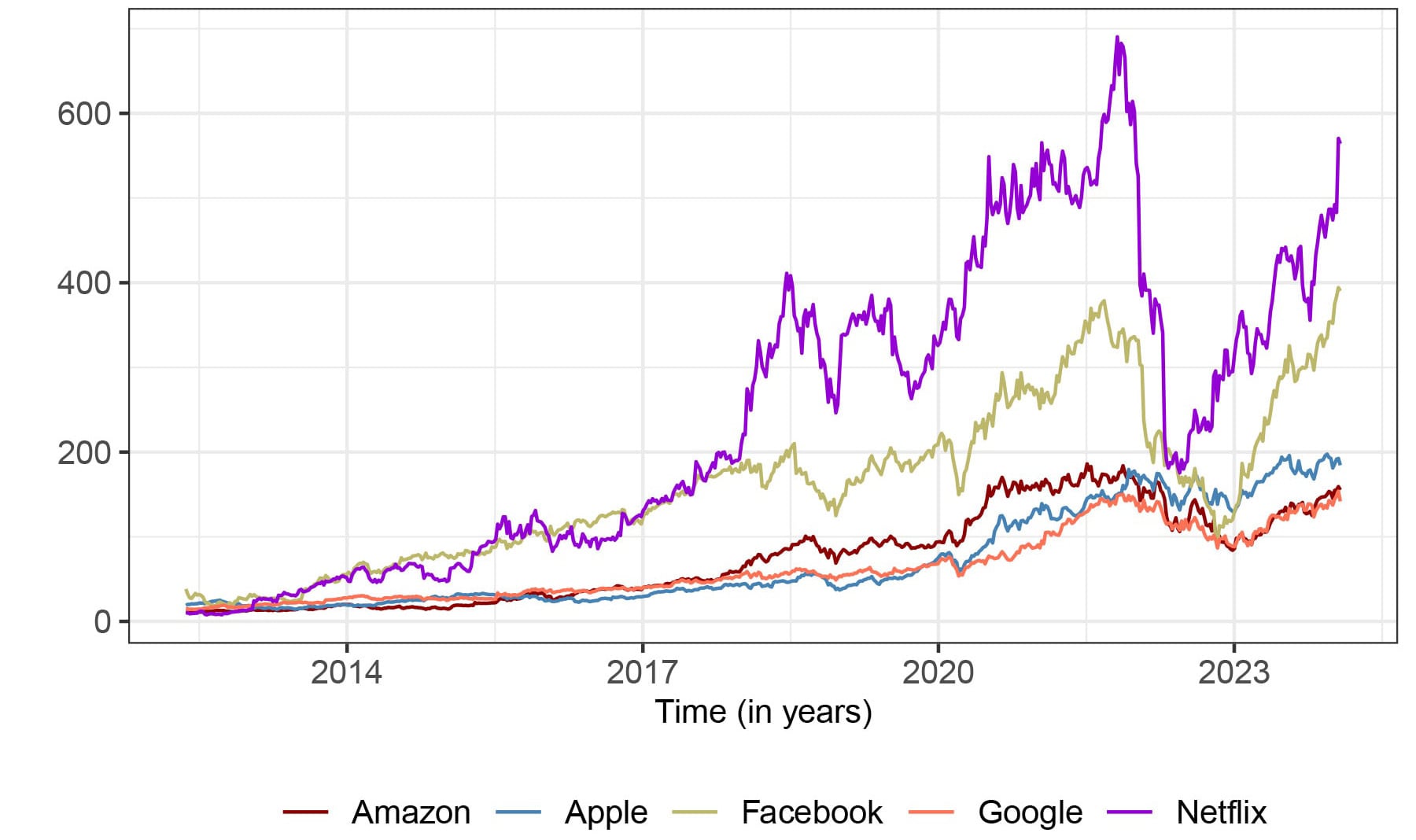

Motivated by this financial landscape, in his paper Prof. de Carvalho shed light on how the combined losses of a set of major AI tech stocks—known as FAANG (Meta’s Facebook, Apple, Amazon, Netflix and Alphabet’s Google)—has been evolving in recent years.

The interest in modelling the extreme losses of FAANG stocks stems from their broad appeal—they attract everyone from everyday investors to major financial institutions—and from their growing role in AI which could increase integration and raise systemic risk.

Adding to the risks mentioned earlier, there is also the traditional risk of herd behaviour according to which investors might irrationally follow market trends or the actions of peers, potentially leading to inflated asset prices and subsequent market bubbles.

Beyond FAANG, the stock market has embraced catchy names acronyms for top AI tech stocks, like The Magnificent Seven (Microsoft, Tesla, Nvidia, and FAANG minus Netflix), and BAT (Baidu, Alibaba, Tencent). While these labels streamline discussions, they also oversimplify the tech sector’s complexity, prompting ‘thinking fast’—akin to Kahneman’s System 1 concept (Montier, 2010; Kahneman, 2011)—which is inadequate for complex decisions in settings like financial markets.

Learning from Data

Stock market comovements (or 'correlations') have been extensively studied in the financial literature; however, relatively little attention has been paid to understanding how stocks move together during periods of financial stress.

The novel method proposed by Prof. de Carvalho enables the assessment of how extreme co-movements in stock returns evolve over time. An application of the proposed methodology to a set of big tech stocks—known as FAANG (Meta’s Facebook, Apple, Amazon,Netflix and Alphabet’s Google)—sheds light on some interesting features on the dynamics of their combined losses over time.

Particularly, the analysis reveals that the relative frequency of extreme joint losses has been higher over 2016–2019, than over the 2020 pandemic outbreak. In particular, the analysis underscores the practical importance of distinguishing between the frequency and the magnitude of extreme losses in stock markets.

Time-varying parameters have a long-standing tradition in Econometrics and Statistics (e.g., Cooley and Prescott, 1976). In line with this tradition, Prof. de Carvalho’s approach captures the temporal dynamics of joint extreme events—specifically their frequency, magnitude, and dependence.

Materials

The data used in the paper are available through the R package DATAstudio. A copy of the manuscript is available from the Oxford University Press website.

References

Cooley, T. F. and Prescott, E. C. (1976), Estimation in the presence of stochastic parameter variation, Econometrica, 167–18

de Carvalho, M. & Palacios Ramirez, K. (2025), Semiparametric Bayesian Modeling of Nonstationary Joint Extremes: How do Big Tech's Extreme Losses Behave? Journal of the Royal Statistical Society, Ser. C, 74, 447–465.

Montier, J. (2010), The Little Book of Behavioral Investing: How Not to be Your Own Worst Enemy, New York: Wiley.

Kahneman, D. (2011), Thinking Fast and Slow, New York: Macmillan.

Financial Times—Editorial Board (2023),How to Prevent AI From Provoking the Next Financial Crisis. Financial Times.